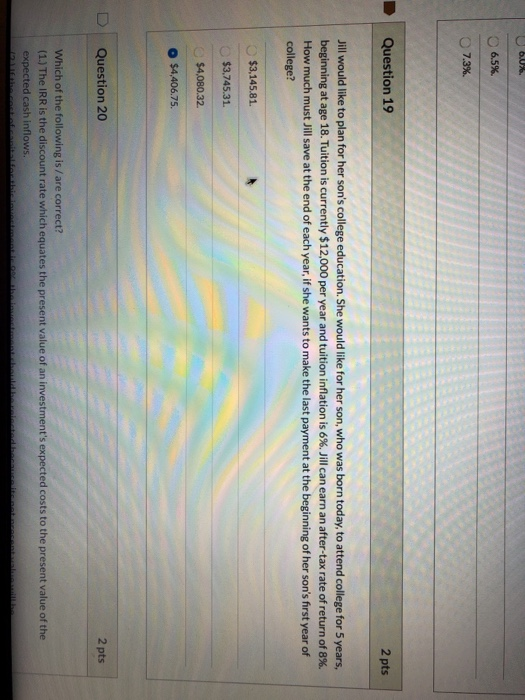

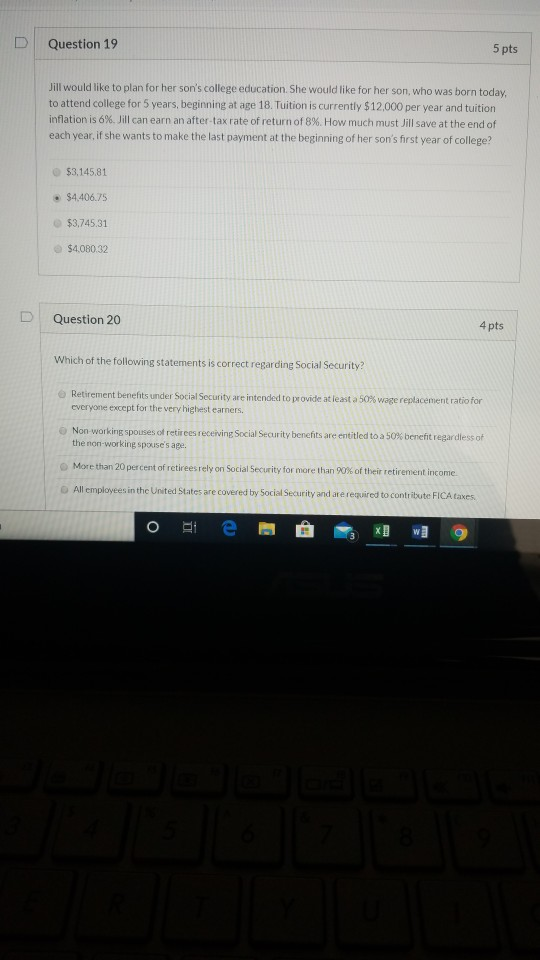

When it comes to personal finance, understanding how to effectively save and invest is crucial for securing a prosperous future. Jill is a prime example of someone who is keen on maximizing her financial growth. With an impressive after-tax rate of return of 8%, she stands at a pivotal point where strategic saving can yield significant dividends. This article delves into the intricacies of how much Jill must save to meet her financial aspirations while navigating the complexities of returns, taxes, and investment options.

Many individuals, like Jill, may find themselves pondering the best methods for achieving their financial goals. Saving is not merely about setting aside money; it involves understanding how to grow those savings efficiently. By exploring Jill's situation, we can uncover valuable insights that can be applied to anyone looking to enhance their financial literacy and investment strategies. The journey to financial independence is often paved with the right information and calculated decisions.

In this discussion, we will address key questions related to Jill's saving strategy, including how her after-tax return influences her savings goals, what factors she should consider when determining her savings rate, and the most effective avenues for investment. Whether you are a seasoned investor or just starting, the principles here can guide you in making informed decisions about your own financial future.

Who is Jill and What are Her Financial Goals?

Jill is a young professional in her early 30s, working in the tech industry. Her financial goals include saving for a down payment on a house, building an emergency fund, and planning for retirement. She is determined to make her money work for her, which is why she is focused on achieving a robust after-tax return on her investments.

What is Jill's Financial Background?

| Detail | Information |

|---|---|

| Name | Jill Smith |

| Age | 32 |

| Occupation | Software Developer |

| Annual Income | $90,000 |

| Current Savings | $20,000 |

| Desired Return Rate | 8% (after tax) |

How Does an 8% After-Tax Rate of Return Affect Jill’s Savings?

The importance of an after-tax rate of return cannot be overstated. This metric represents the actual earnings Jill can keep after accounting for taxes on her investments. If Jill can consistently earn an 8% return, she will be able to reach her financial goals faster than if she were to settle for lower returns. But how much must Jill save to achieve these goals with such a return?

What Factors Should Jill Consider When Saving?

- Investment Options: Jill should evaluate different investment vehicles, such as stocks, bonds, and mutual funds, to identify those that can yield the desired return.

- Tax Implications: Understanding how different investments are taxed will help Jill maximize her after-tax return.

- Time Horizon: The length of time Jill plans to save before making withdrawals will significantly impact her investment decisions.

- Risk Tolerance: Jill must assess her comfort level with risk to determine which investments align with her financial goals.

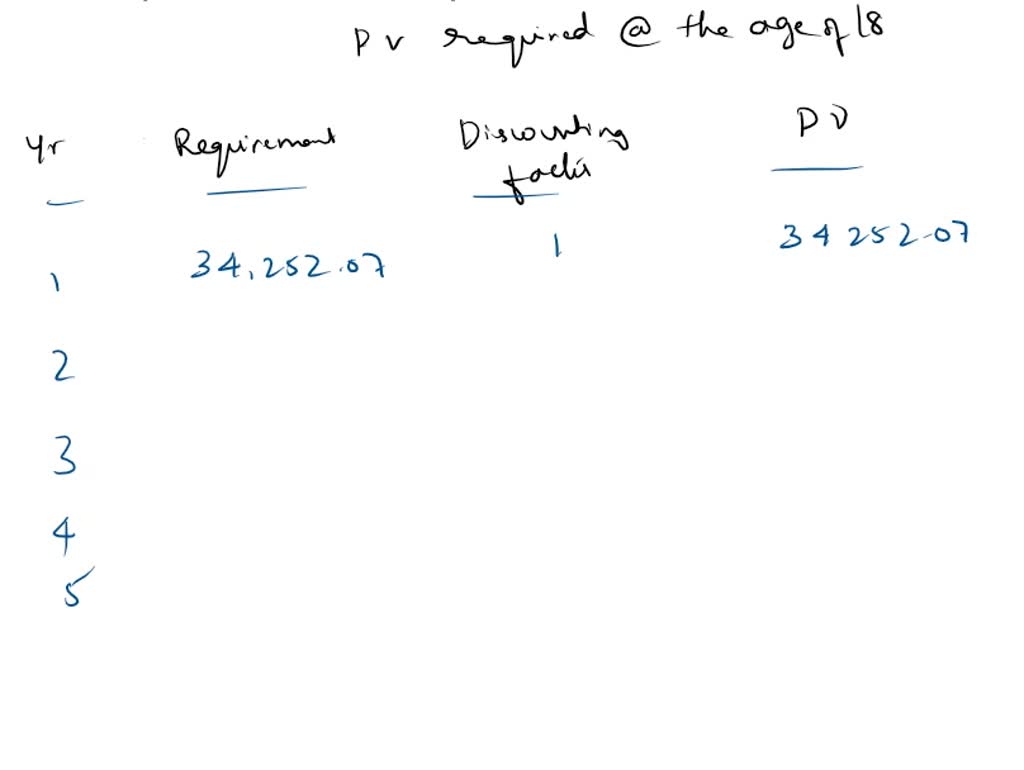

How Much Must Jill Save to Achieve Her Goals?

To determine how much Jill must save, we can use the future value of an annuity formula, which calculates how much she needs to contribute regularly to reach her target amount. For example, if Jill aims to save $100,000 in 10 years with an 8% return, she can calculate her monthly savings using the following formula:

What is the Future Value of an Annuity Formula?

The formula for the future value of an annuity is:

FV = P × [(1 + r)^n - 1] / r

Where:

- FV = future value of the annuity

- P = payment amount per period

- r = interest rate per period

- n = total number of payments

How Can Jill Determine Her Monthly Savings Requirement?

To find out how much Jill must save monthly, she can rearrange the formula to solve for P:

P = FV × r / [(1 + r)^n - 1]

For Jill’s goal of $100,000 in 10 years (120 months) with an 8% annual return (0.08/12 per month), the calculation would look like this:

What Are the Steps Jill Needs to Take to Calculate Her Monthly Savings?

- Convert the annual interest rate to a monthly rate: 0.08 / 12 = 0.00667

- Determine the total number of periods: 10 years × 12 months/year = 120 months

- Apply the values to the formula to calculate P.

After performing the calculations, Jill will discover exactly how much she needs to save each month to achieve her savings goal of $100,000 in 10 years.

What Other Strategies Can Jill Implement to Enhance Her Savings?

In addition to regular savings, Jill can adopt several strategies to increase her wealth:

- Automate Savings: Setting up automatic transfers to her savings or investment accounts can ensure consistency.

- Diversify Investments: By spreading her investments across various assets, Jill can mitigate risks and potentially enhance returns.

- Maximize Retirement Accounts: Contributing to retirement accounts like 401(k)s or IRAs can offer tax advantages and help grow her savings.

- Reduce Expenses: Analyzing and adjusting her budget can free up more money for savings.

Conclusion: How Can Jill Align Her Savings Strategy with Her Financial Goals?

Jill can earn an after-tax rate of return of 8%. How much must Jill save at regular intervals to reach her financial goals? By carefully calculating her savings requirements, considering her investment options, and implementing effective strategies, Jill is well on her way to achieving her dreams. As she navigates the financial landscape, her proactive approach to saving and investing will undoubtedly lead her towards a secure and prosperous future.