In our increasingly complex financial world, uncertainty looms large over individual investors and consumers alike. The financial system, however, is designed with multiple layers of protection that work to minimize this inherent risk. From banking institutions to insurance companies, each component of the financial system plays a vital role in ensuring that individuals are safeguarded against financial calamities. Understanding how these systems function can empower individuals to make informed decisions about their finances while enhancing their overall security.

At its core, the financial system creates an environment where resources are allocated efficiently, and risks are spread across various entities. This minimizes the impact of financial loss on any single individual. By pooling risks through mechanisms like insurance and investment funds, the financial system not only protects individual assets but also fosters economic growth. In essence, the financial system works as a safety net, cushioning individuals from the unpredictability of market fluctuations and personal financial misfortunes.

The interconnectedness of financial institutions also plays a crucial role in risk management. By distributing financial resources and risks, the system creates a buffer against individual failures. Whether through diversified investment portfolios or federally insured deposits, these mechanisms ensure that individuals can weather financial storms with greater resilience. As we delve deeper into the workings of the financial system, we will uncover the various ways it minimizes individual risk and promotes financial stability.

What Are the Key Components of the Financial System?

The financial system comprises several key components, each serving a distinct purpose in minimizing individual risk:

- Banking Institutions

- Insurance Companies

- Investment Firms

- Regulatory Bodies

How Do Banking Institutions Protect Individual Assets?

Banking institutions are often the first line of defense in protecting individual assets. They provide a secure place for individuals to deposit their savings, and these deposits are typically insured up to a certain limit. This insurance means that in the event of a bank failure, individuals can recover their funds, minimizing their risk of total loss. Furthermore, banks offer various financial products that allow individuals to diversify their investments, thus reducing individual exposure to any single asset class.

Are There Different Types of Bank Accounts for Risk Management?

Yes, there are various types of bank accounts designed to cater to different financial needs and risk profiles:

- Checking Accounts: Provide liquidity for daily transactions.

- Savings Accounts: Offer interest on deposits while maintaining easy access.

- Certificates of Deposit (CDs): Lock in funds for a fixed term with higher interest rates.

What Role Do Insurance Companies Play in Risk Mitigation?

Insurance companies are pivotal in the financial system's risk management framework. They provide protection against unforeseen events such as accidents, health issues, or property damage. By paying a premium, individuals transfer the financial risk of these events to the insurance company. In doing so, they can avoid potentially devastating financial losses that could arise from unexpected circumstances.

How Does Risk Pooling Work in Insurance?

Risk pooling is a fundamental principle in insurance. By gathering a large number of policyholders, insurance companies can spread the risk across a wider base. This means that while some individuals may experience losses, the majority will not, allowing the insurer to pay out claims without jeopardizing their financial stability. This collective approach significantly minimizes individual risk.

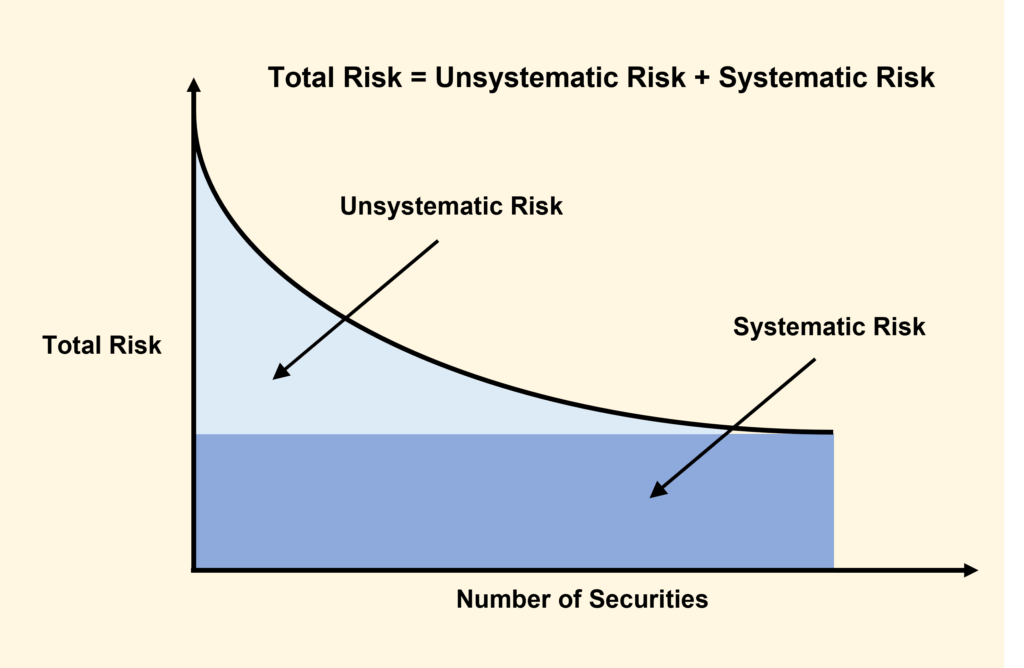

How Do Investment Firms Help to Diversify Risk?

Investment firms play a crucial role in helping individuals manage their investment risks. By offering a variety of investment products, including mutual funds and exchange-traded funds (ETFs), these firms enable investors to diversify their portfolios. Diversification is one of the most effective strategies for minimizing risk, as it spreads investments across different asset classes, sectors, and geographical regions.

What Is the Importance of Asset Allocation in Risk Management?

Asset allocation refers to the process of dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash. This strategy is essential for risk management because it helps to balance potential returns with the level of risk an investor is willing to accept. By carefully considering their asset allocation, individuals can tailor their investments to achieve their financial goals while minimizing individual risk.

How Do Regulatory Bodies Enhance Financial System Stability?

Regulatory bodies play a critical role in overseeing the financial system to ensure its stability and integrity. Agencies such as the Federal Reserve and the Securities and Exchange Commission (SEC) impose regulations that protect consumers and maintain confidence in the financial markets. By enforcing transparency and ethical behavior among financial institutions, regulatory bodies help to minimize the risk of fraud and systemic crises.

What Are Some Examples of Regulatory Measures?

Some examples of regulatory measures include:

- Capital requirements for banks to ensure they can absorb losses.

- Consumer protection laws to safeguard individuals from predatory practices.

- Regular audits and examinations of financial institutions to ensure compliance.

Why Is Financial Literacy Important in Risk Management?

Finally, financial literacy is crucial for individuals seeking to minimize their financial risks. Understanding the tools and mechanisms available within the financial system empowers individuals to make informed decisions. By educating themselves about budgeting, investing, and insurance, individuals can better navigate their financial journeys and protect themselves from potential pitfalls.

How Can Individuals Improve Their Financial Literacy?

Improving financial literacy can be achieved through various means:

- Attending workshops or seminars on personal finance.

- Utilizing online resources and courses to learn about investing and risk management.

- Consulting with financial advisors for personalized guidance.

Conclusion: The Financial System as a Safety Net

In conclusion, the financial system minimizes individual risk through a combination of banking institutions, insurance companies, investment firms, and regulatory bodies. Each of these components contributes to a robust framework that protects individuals from financial uncertainties. By understanding these mechanisms and enhancing their financial literacy, individuals can navigate the financial landscape with confidence and security, effectively minimizing their risks. To summarize, the financial system plays a vital role in protecting individuals and ensuring economic stability, making it essential for everyone to engage with it actively and knowledgeably.